Insert here your custom code

Need instant 10,00,000/- Loan ?

How Does Age Affect Personal Loan Eligibility?

When you think about applying for a personal loan, the first question that often comes to mind is — “Am I eligible?” While factors like income, employment type, and credit score matter, one of the most crucial factors lenders look at is your age. Yes, your age can significantly influence your personal loan eligibility. Let’s understand why age matters, how banks evaluate it, and how you can improve your chances of getting approved for the loan you need. Why Age Matters in Personal Loan Approval When banks or NBFCs offer personal loans, they assess the applicant’s ability to repay the borrowed amount. Age acts as an indicator of both financial stability and repayment capacity. Think of it this way: - A younger applicant (say, 21–25 years old) may have a limited credit history and a shorter work experience, which makes them slightly riskier for lenders. - A middle-aged applicant (between 26–50 years) is usually considered ideal — they’re financially stable, employed, and often have a consistent repayment record. - An older applicant nearing retirement may face limitations in tenure or loan amount because their income potential may reduce soon. This is why lenders have a defined age bracket for personal loans, usually between 21 to 60 years (and sometimes up to 65 for salaried individuals or self-employed professionals). Typical Age-Based Loan Eligibility Criteria Each financial institution in India has its own set of personal loan eligibility criteria, and age is one of the key factors among them. Generally, most banks and NBFCs offer personal loans to applicants within a specific age range to ensure repayment feasibility. For salaried individuals, the minimum age requirement is usually 21 years, while the maximum age allowed at the time of loan maturity is around 60 years. For self-employed professionals, the maximum age limit can extend up to 65 years, as they often have a longer earning span. This means that even if you meet all other conditions such as income stability or a good credit score, your loan application may still be rejected or approved for a lower amount if you fall outside these defined age limits. How Age Affects Loan Amount & Tenure Age doesn’t just determine whether you can get a loan — it also affects how much you can borrow and for how long. Loan Tenure Younger applicants can often choose longer tenures — for example, 5 years or more — since lenders believe they’ll have steady income for a longer time. On the other hand, someone closer to 60 years of age may only get a tenure of 1–3 years because their employment years are limited. Loan Amount Your age indirectly affects your income level and financial commitments. A 28-year-old IT professional earning ₹70,000/month can easily qualify for a ₹5 lakhs personal loan eligibility, while a 58-year-old nearing retirement might get a smaller amount due to lower repayment duration. Interest Rate Younger borrowers with good credit scores might enjoy lower interest rates, whereas older applicants may be offered slightly higher rates due to perceived repayment risks.

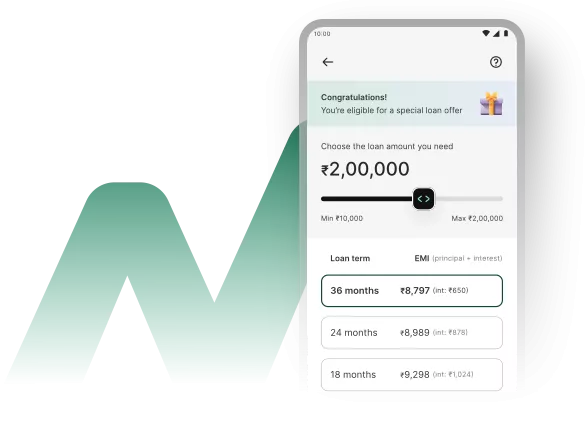

How to Check Personal Loan Eligibility Easily Today, you don’t need to visit a bank branch to know if you’re eligible. You can simply use a personal loan eligibility calculator available on most lender websites. This online tool helps you estimate the loan amount, tenure, and EMI you can get based on your income, age, and credit score. Here’s how to use it: 1. Visit a lender’s website (like Fundcera, Indian Bank, or Money View). 2. Find the personal loan eligibility check online section. 3. Enter your age, income, employment type, and existing loan details. 4. The calculator instantly shows your eligible loan amount and expected EMI. This quick step gives you a fair idea of whether your age and financial profile meet the lender’s personal loan eligibility criteria before you apply. Age-Based Example: How Different Banks Handle It Let’s look at how a few financial institutions view age when offering personal loans. 1. Indian Bank Personal Loan Eligibility Indian Bank typically allows personal loans to salaried individuals between 21 and 60 years. For self-employed professionals, the maximum age can extend to 65 years at the time of loan maturity. A steady income source is mandatory, and younger applicants with limited experience might need a guarantor. 2. Money View Personal Loan Eligibility Money View, a leading Fintech platform, offers quick approval and flexible eligibility criteria. Applicants between 21 to 57 years are eligible, provided they have a minimum monthly income of ₹13,500 and a valid bank account. The platform uses its personal loan eligibility check online system to assess age, income, and creditworthiness instantly. 3. Home Credit Personal Loan Eligibility Home Credit focuses on easy access and digital approval. Their home Credit personal loan eligibility includes applicants aged 19 to 65 years with a steady income source. They also use AI-based credit checks to evaluate your repayment capacity — where age plays a key role. Tips to Improve Your Personal Loan Eligibility Regardless of Age Even though age influences your loan approval chances, there are practical ways to improve your eligibility: 1. Maintain a Strong Credit Score: A CIBIL score of 700+ can balance out age-related disadvantages, especially for younger or older applicants. 2. Show a Stable Income: Provide income proof like salary slips, ITRs, or bank statements to show consistent earnings. 3. Opt for a Shorter Tenure: If you’re nearing retirement, choosing a shorter loan tenure can increase your chances of approval. 4. Add a Co-Applicant: A younger co-applicant or guarantor with stable income can strengthen your personal loan eligibility. 5. Use a Personal Loan Eligibility Calculator: Always use this tool to check your eligibility online before applying. It prevents unnecessary rejections that could affect your credit score. Real-Life Example Let’s say Ramesh, aged 28, earns ₹60,000/month and works in a private company. Using a personal loan eligibility calculator, he discovers he qualifies for a ₹5 lakh personal loan for 5 years at 11% interest. Meanwhile, Suresh, aged 56, with the same income, qualifies for only ₹2 lakh over 2 years due to his age and shorter tenure window. Both have good credit scores, but age becomes the deciding factor in the loan amount and duration. This example shows why understanding how age impacts your personal loan eligibility is crucial before applying. Final Thoughts Age plays a much bigger role in personal loan eligibility than most people realize. It influences how much you can borrow, your repayment tenure, and even your interest rate. However, you can still get the loan you need by: - Maintaining good financial discipline - Using a personal loan eligibility calculator to plan ahead - Applying with the right lender that fits your age and income bracket So, before submitting your next loan application, take a minute to check your personal loan eligibility online. Whether you’re 25 or 55, smart planning and transparent banking can help you achieve your financial goals smoothly.

Empowering your financial journey with seamless Self-Apply Loan Options and dedicated Loan Agent Assistance, all integrated into smart, value-packed Subscription Plans.

Experience transparency, speed, and personalized support—only at Consult.Fundcera.com

GST : 24AAGCF2801F1Z6

CIN : U66190GJ2025PTC159913

Ready To Apply?

We make finance possible in just 3 simple steps to provide a fast, flexible and friendly customer experience

@copyright 2025 Fundcera | Privacy Policy

.webp)

.webp)

.webp)

.webp)