Insert here your custom code

Need instant 10,00,000/- Loan ?

Smart Ways to Compare Interest Rates, Tenure & EMIs

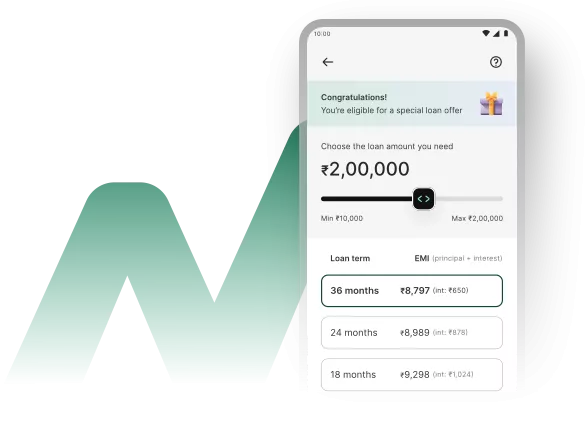

When it comes to borrowing money—especially for big financial goals like buying a home, funding higher education, or consolidating debt—your loan decision is one of the most important financial choices you will ever make. The three pillars of any loan are interest rates, loan tenure, and EMI structure. Understanding how they work, and more importantly, how they impact your budget in the long run, can save you from years of financial stress. In this blog, we’ll break down each factor in simple language and share smart ways to compare loans so that you can make the right choice. 1. Why Comparing Loans is Crucial Most people look only at the interest rate when applying for a loan. While that’s important, it’s only one piece of the puzzle. The tenure (duration of repayment) and the EMI (Equated Monthly Installment) structure also play an equally significant role. Here’s why comparison matters: - A small difference of 0.5% in interest rate can save (or cost) you lakhs of rupees over the loan period. - Choosing the wrong tenure may lead to either unaffordable monthly payments or paying way too much in total interest. - Not all EMIs are the same—some loans allow flexibility, while others lock you into rigid structures. In short, comparing thoroughly before signing the dotted line is the key to financial peace of mind. 2. Understanding Interest Rates Interest is the cost of borrowing money, and it comes in two main types: Fixed Interest Rate - Remains the same throughout the loan tenure. - EMI does not change, making budgeting easier. - Good for people who prefer stability and don’t want surprises. - Example: If your loan interest is 9% fixed, it stays 9% for the entire tenure. Floating Interest Rate - Varies depending on market conditions and RBI’s repo rate. - EMIs can go up or down during the loan period. - Generally, floating rates are lower than fixed rates at the start. - Best for borrowers who can handle some fluctuations and hope to benefit from lower rates in the future. Smart Tip: If interest rates are high when you borrow, choose floating rates. If rates are low and expected to rise, go for fixed rates. 3. Loan Tenure: Short vs. Long Tenure simply means the time you take to repay the loan. Short Tenure Loans - Higher EMIs every month. - Total interest paid is much lower. - Suitable if your income is high and you want to get debt-free quickly. Long Tenure Loans - Lower EMIs every month, making repayment easier on your monthly budget. - But the total interest you pay over time is much higher. - Good if you want breathing space in your monthly expenses. Smart Tip: If you can afford slightly higher EMIs without affecting your lifestyle, always choose a shorter tenure. It saves you huge money in the long run. 4. EMI Structures Your EMI = Principal + Interest, divided over the loan tenure. But did you know that there are different types of EMI options? Standard EMI The same EMI every month until the loan is closed. This is the most common structure. Step-Up EMI EMIs start lower and gradually increase. Good for young professionals whose income is expected to rise over time. Step-Down EMI EMIs start higher and reduce with time. Useful for people who may have a strong income now but expect expenses to rise in the future (e.g., nearing retirement). Flexible Prepayment Options Some lenders allow you to pay extra when you have surplus funds. This reduces your principal and cuts down interest. Always check prepayment penalties before signing. Smart Tip: If you’re early in your career, a step-up EMI may work well. If you want predictability, stick to standard EMIs.

5. How to Compare Loans Smartly Here are some practical steps to compare loan offers like a pro: Compare APR, Not Just Interest Rate The Annual Percentage Rate (APR) includes not only the interest rate but also processing fees, administrative charges, and insurance premiums. A loan with a lower interest but higher fees may actually cost you more. Use Online EMI Calculators Before finalizing a loan, use an EMI calculator to test different combinations of interest rate, tenure, and loan amount. This gives a clear idea of how much you’ll pay monthly and in total. Check Flexibility Does the lender allow part-prepayment or foreclosure without penalties? The ability to repay early can save you a fortune in interest. Look Beyond Banks Don’t limit yourself to just one or two banks. Compare offers from NBFCs (Non-Banking Financial Companies), digital lenders, and credit unions. They may have competitive rates and faster approvals. Assess Your Own Financial Health Don’t take the maximum loan just because you are eligible. Borrow only what you truly need and can repay comfortably. A safe rule is to keep EMIs within 30–40% of your monthly income. 6. Real-Life Example Let’s say you borrow ₹20,00,000 for 20 years. - At 9% fixed rate: EMI ≈ ₹18,000, total interest ≈ ₹23,00,000. - At 9% floating (average 8% over tenure): EMI ≈ ₹16,700, total interest ≈ ₹20,00,000. - Same loan with 10 years tenure: EMI ≈ ₹25,000, total interest ≈ ₹10,00,000. The difference is huge! By choosing wisely, you can save lakhs of rupees. 7. Common Mistakes to Avoid - Only looking at EMI without checking total cost. - Ignoring hidden charges like processing fees. - Choosing maximum tenure just for comfort. - Not comparing different lenders. - Skipping terms & conditions (especially prepayment rules). 8. Final Thoughts Loans are powerful financial tools when chosen wisely, but they can become lifelong burdens if selected carelessly. Always remember: - Compare fixed vs floating interest rates carefully. - Choose a tenure that balances affordability and total cost. - Pick an EMI structure that matches your financial situation. - Use online calculators, read fine print, and never hesitate to ask questions. Making a smart decision today can save you years of stress tomorrow.

Empowering your financial journey with seamless Self-Apply Loan Options and dedicated Loan Agent Assistance, all integrated into smart, value-packed Subscription Plans.

Experience transparency, speed, and personalized support—only at Consult.Fundcera.com

GST : 24AAGCF2801F1Z6

CIN : U66190GJ2025PTC159913

Ready To Apply?

We make finance possible in just 3 simple steps to provide a fast, flexible and friendly customer experience

@copyright 2025 Fundcera | Privacy Policy

.webp)

.webp)

.webp)

.webp)